I can't believe it's April already! Bear with me, this is a long one.

March spending was a touch lower than Feb...by ~$100....still would like to get this down, but also happy that I am finding balance, and a way to live life in a satisfying way without derailing my debt pay down efforts. This spending does not include housing or debt pay down (basically any of my bills) - this is all "discretionary" spending....quotes because buying groceries isn't exactly discretionary lol. But it's something I have control over rather than my mortgage, etc.

Alcohol - 0

Car/Gas - $60.20 (got gas twice this month. Once because I needed it, and once because I was killing time and was near the cheaper gas station. Might be able to get through April without getting it again but not sure if I have any plans that include longer drives than usual.)

Clothing - $45.30 (this was in conjunction with a $20 birthday reward I received from a store I used to shop at a lot. I don't remember which of my snowflakes was used to fund the out of pocket spending, but thems be my rules.)

Dining/Entertainment - $125.59 (this was extraordinarily high for me lately. I don't really order takeout or go out to dinner, but there were a few things lumped pretty close together. Big contrast from last month's $2.06 haha.)

Education - $50 (enrollment fee for school. It's getting real!)

Gifts - $117.05 (Mom birthday gift)

Grocery/Household/Toiletries - $529.71 (by far my biggest category. It was a slightly spendy month on groceries alone, then I had a few other things that get categorized in here as well. I would like this to be under $500 or better for April.)

Medical - 0 (although I am expecting a bill for the copay for my appt last week with the plastic surgeon - this will be captured whenever they send it/I pay it.)

Miscellaneous - ($98.14) (this is negative because it's offset by payment of my wellness stipend. Can't remember what else ended up in here.)

Office Supplies - ($10.84) (also negative, got a credit from Staples for them losing the delivery of my ink at the end of Feb.....credit posted in March.)

Personal Care - 0

Pet - $116.34 (this should cover the majority of my "start up" costs for taking my cats, I still need carriers. I'll have to start buying food & litter end of May/early June, Mom is providing the first month's supply.)

Grand Total - $978.14 (overall ok. I did have to dip into savings for a few things, but I'd rather do that then put anything on a credit card.)

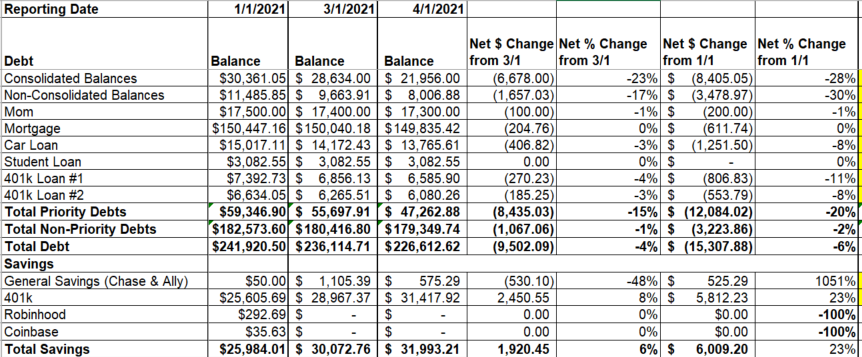

Month End Summary - below's pic is a screenshot from my tracker on where things stand, measured in both the change from 1/1 and the change from 3/1. Note, 401k loans and balance do not include the payments/contributions from my 3/31 paycheck, they take a few days to post to the account.

Overall everything is going in the right direction! Debt is going down, especially the priority debts. Savings is still going up, even if there was a downturn along the way. Very pleased with my progress.

Since today marks the start of the second quarter, I wanted to do a check in on my goals for the year and how I am tracking against them so far. I went back to my post from the beginning of the year to see what I said...

Consolidated Balances: In early January, the consolidated balances left to be tackled were 9 of the original 12 (3 having reached payment agreements and in active repayment). As of today, there are 5 left to be tackled. Of the 7 that an agreement was made, 6 are currently in active repyament and 1 has been paid. The goal was: stay the course and hope that the balance was down to around $20k by end of year. As of today, it is just under $22k. I would estimate that 2 more of the accounts will reach payment agreements this year, leaving me with 3 to go and a balance of about $16k if my estimates on what will be handled next are correct - if I'm wrong, it'll be even better. Ahead of goal there for sure.

Non-Consolidated Balances: these are my credit cards that did not go into the program. There are 6 of them, 5 of which had balances as of Jan 1. My goal was to pay off 3 of them by the end of the year, and bring my starting balance of ~$11k to ~$5k. As of today, I have paid off the 3 I wanted to have handled by end of year. Current balance remaining is just at $8k. Based on planned regular payments alone, I'll be just about there. That doesn't include some larger irregular payments I have coming in throughout the year that will be directed here, and whatever extra I am able to scrape up to chip away at that. I didn't state this goal here, but I also said elsewhere that I wanted my main credit card (the one with the highest balance) to be at or under 75% utilization by the end of the year - based on planned payments alone, it's projecting to be around 50% by EOY, with potential to be under 25% if certain events that trigger a snowflake come into play. Ahead of goal there as well!

Mom debt: my goal here was just to start paying this back. As of this writing, I have made 2 payments, and incorporated it into my monthly budget. I will not make much progress this year, but it was more about the intention than the measurable progress. I will increase this next year as other debt is paid off/my salary increases. On track.

Non-priority debt: goal was to continue to service on normal schedule. Not much to say here, as I've continued making regular payments to these - mortgage, car loan, 401k loans. Student loans will remain in deferment until after I graduate....even if the federal deferment is not extended again, which I think it will be, by that time I will be a full time student which automatically puts them in deferment. I will be adding to my student loan balances, but this is good debt so I am ok with it. For now, these are all "make the payment on time." On track.

A secondary goal under this heading was to potentially refinance my mortgage at the end of this year or beginning of next, but I've changed my mind on that. I was hoping to pull out some equity to cover my plastic surgery, but I can't be sure of how much I actually have without paying for an appraisal. Based on my purchase price, I have $50k of equity, or 25%. To fund surgery, I would need that to be $80k of equity (not impossible, my apartment was very underpriced in my opinion because it needed a gut renovation which I did), plus pay closing costs etc. I have since decided that I'm going to take another 401k loan (have to pay off one of the existing ones first, but I have a plan because I always have a plan). This also makes the debt shorter term, it would be paid off in 5 years or less. Plus, I have decided I'm going to move in a few years so it doesn't seem worth it to refinance just to go on and sell in 3-4 years. All works in progress. I'll talk about them in another post when I get closer to pulling the trigger.

Grow savings: I started the year with $50 in cash savings. No, that's not a typo. It was a scary place to be. The goal was to be somewhere around $2k in cash savings by end of year. I managed to get up as high as $1100 at one point, had to pull some out, and am currently sitting at just under $600 not including some snowflake money that is in transit. This goal is on track.

Bump retirement savings: I started the year contributing 10% to my 401k, and the goal was to increase that to 12% by midyear. Not sure if I will be able to do this by midyear, but it will definitely happen sometime this year. This does not include my company match, in which I will be fully vested next month. I currently have 2 401k loans, which are paid via auto deductions from my paycheck. As mentioned above, I am planning to pay one of these off by end of year, and take out another loan to fund surgery. I don't want to remain in the habit of borrowing from my future to pay for things, but I am hopeful that by the next time something of this importance comes up, I will be in a different financial position and have more options. On track based on planning but we will see.

Investments: I started the year with small balances at Coinbase (~$30) and Robinhood (~$300). The goal was to throw extra money at them as able, without any sort of measurable amount stated. I ultimately decided that in my situation, that money would be better used elsewhere, so I cleared those accounts out. I guess technically this goal will not be met, but in a conscious way haha.

Get promoted (financial and non-financial): Has not happened yet but I have a good feeling for either July or October! When this happens, once I know what my salary increase will be, the first thing I will do is fund a grocery budget in paychecks lol. The second thing will be to increase 401k contribution, and the third will be to start moderately funding sinking funds. After that, I will likely focus any extra money on debt.

Other non-financial goals: there were 2 goals here. One was to continue to stay focused on my weight loss journey. No measurable goal here at that point, but I have since confirmed my goal weight - well, my plastic surgeon set it for me haha. He wanted me to lose 20-25 pounds from where I was as of last week in order to proceed with surgery. I am hoping as a strech goal to start surgeries (need two rounds) in December, so would need to achieve this before then. I set an interim goal of losing ~10-15 pounds from where I was last week by my next appointment with him at the end of June, which is not only a big milestone for me (2 milestones actually), but is halfway to where he wants me to be. As of today, I am 8-13 pounds from the interim goal with just under 3 months to go. I'm feeling hopeful. The second goal here was to start taking steps for plastics. Clearly that's happening haha. I've met with 4 surgeons to date, and am undecided if I will meet with more, or if I have my guy. I've also come up with a pretty detailed plan to pay for it. Both of these goals are on track, if not ahead of schedule.

Overall, I think I'm killin' it and could not be more pleased with my progress. I don't feel deprived in any way, and having to be creative to fund wants from extra money has made me think a little more deeply about whether or not something is worth the effort to get it (I used to just buy and think about it later). I appreciate the things I do end up buying more now.

This year is really all about laying the foundation for a very ambitious 3 year plan. I'm confident that I will achieve this plan based on my mindset thus far. None of this feels difficult or a slog. And in the end, the position I will be in will be amazing.

April 2nd, 2021 at 12:11 am 1617322282

April 2nd, 2021 at 12:25 am 1617323101